$2 billion real estate developer and senior living provider

Summary

Unable to pay its bills and under investigation by the SEC and the State of Oregon for fraudulent investment practices, misuse of cash, and other securities violations, Sunwest Management engaged Hamstreet & Associates as CRO to close a challenging asset sale, repair operations, restructure debt, and return the company to sound financial footing. This unique case involved sophisticated tax and investment structures, a federal equity receivership, substantive consolidation through chapter 11, and two large sale transactions—the second a $1.3 billion acquisition of Sunwest’s core operations by an affiliate of The Blackstone Group.

The Background

The prospects of missing payroll or losing vendor supplies of food and utilities to support thousands of elderly residents were real threats

At its peak in 2007, Sunwest Management was the largest privately-held senior living provider in the country with more than 290 senior living communities in 38 states, in addition to scores of other diverse real estate assets across the country. Financed by traditional mortgage lending and a complicated investment program based on tax-sheltered contributions from tenant-in-common co-owners, the company grew rapidly during the real estate boom years, was significantly overleveraged, and depended on the continued rise in real estate values and a constant cycle of refinancing to generate cash flow for debt service and guaranteed investor payments. With the tightening of the credit markets in 2007 Sunwest entered a period of severe crisis. When Hamstreet & Associates came on board as Chief Restructuring Officer and advisors in November 2008, Sunwest had defaulted on approximately $1 billion of debt, halted most loan and investor payments, and deeply antagonized its 100 lenders and 1,500 investors.

The Challenge

Sunwest’s cash crisis was the most extreme ever seen by the Hamstreet & Associates team. The prospects of missing payroll or losing vendor supplies of food and utilities to support thousands of elderly residents were real threats for the first three months of the engagement. Sunwest’s secured lenders were fatigued and hostile towards the company due to extended lack of payment, improper cash management practices, lack of forthright communication and default on forbearance agreements.

Many lenders were putting receivers in place and pursuing foreclosure. At a minimum, the banks insisted on lock boxes. Most resisted new forbearance agreements that would give the company a chance to restructure.

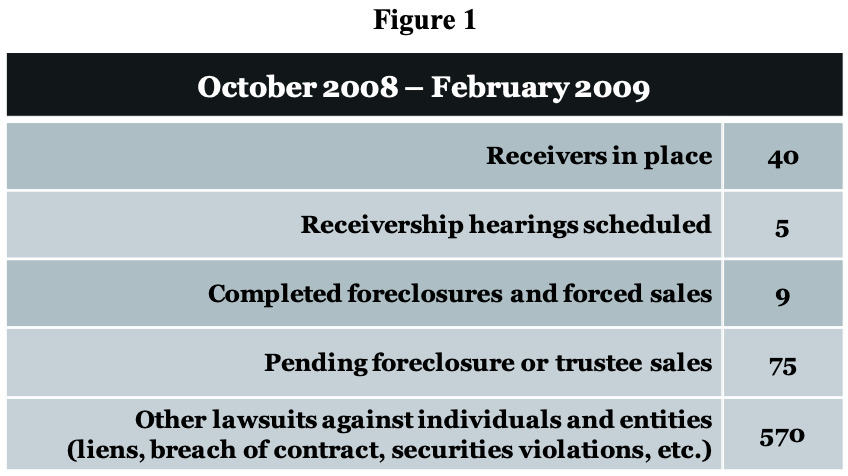

By mid-January 2009 Sunwest and its principals were subject to more than 600 lawsuits for foreclosure, receivers, liens, breach of contract, securities violations, and other causes of action (Fig. 1). The company was also under investigation by the SEC for improperly commingling cash among its 750+ separately-owned legal entities, raising investor funds without proper disclosures, and misusing investment monies.

Under Hamstreet’s leadership, company personnel responded enthusiastically, as demonstrated by positive employee and resident satisfaction surveys, a sharp decline in the number of regulatory issues, and improvement in operational and financial performance.

On the positive side, a sale of 45 prime senior living assets was in the works, with a pledge from three Sunwest principals to support the turnaround with their $30 million share of the proceeds. But closing this transaction depended on consents from outside investors who were angry and deeply mistrustful of the company. And when Sunwest’s founder filed for personal bankruptcy prior to the sale, access to his share of the proceeds—by far the largest portion of those pledged—fell into doubt.

The company’s complex ownership and investment structures created an additional layer of difficulty. Sunwest’s three principal owners held controlling interests in most of the company’s affiliated entities, but the extent of their interests and the remainder of the ownership picture varied by entity. Sunwest had resources to protect only a small number of its assets in chapter 11. Meanwhile, the complex tax shelters underlying the ownership structures meant that investors had more than just their cash at stake; anxiety over tax issues made for an extremely vocal investor community that sought to (and did) play an active role in the case.

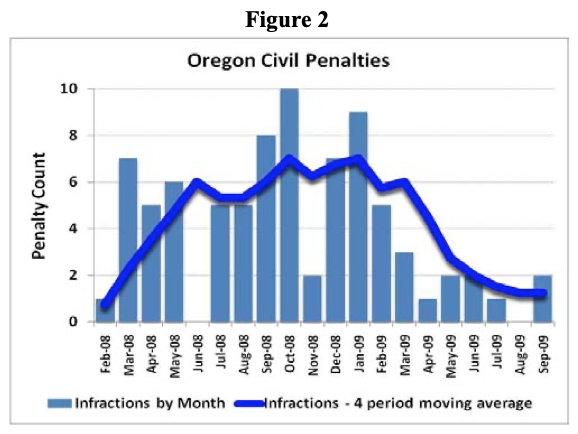

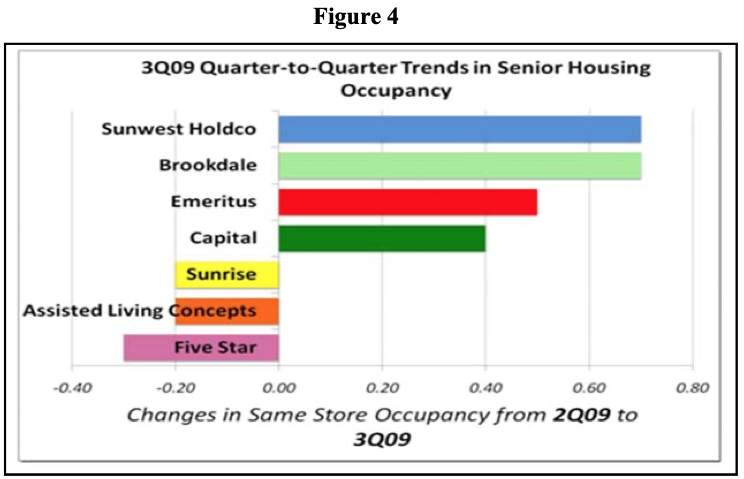

A second, simultaneous initiative was the repair and improvement of Sunwest’s core operations. At the outset of the engagement Hamstreet & Associates appointed an operational specialist with oversight of Sunwest’s Chief Operating Officer. Under this leadership, Sunwest improved management training and employee incentive programs, quality control, and the measurement and fulfillment of performance benchmarks. Company personnel responded enthusiastically, as demonstrated by positive employee and resident satisfaction surveys, a sharp decline in the number of regulatory issues (Figure 2), and gradual improvement in operational and financial performance (Figure 3). During a difficult time in the senior housing market Sunwest’s core assets performed on a par with or better than industry leaders (Figure 4).

The Results

Hamstreet & Associates took immediate steps to control cash, introduce proper cash management practices, persuade lenders to enter new forbearance agreements, and file chapter 11 proceedings for 26 valuable communities at high risk of foreclosure. Alongside these ongoing efforts, the firm’s first major achievement was to close the $364 million asset sale and then, after mediation with investor and creditor committees in the Sunwest founder’s personal bankruptcy, win the right to use his share of the proceeds to restructure the company.

A second, simultaneous initiative was the repair and improvement of Sunwest’s core operations. At the outset of the engagement Hamstreet & Associates appointed an operational specialist with oversight of Sunwest’s Chief Operating Officer. Under this leadership, Sunwest improved management training and employee incentive programs, quality control, and the measurement and fulfillment of performance benchmarks. Company personnel responded enthusiastically, as demonstrated by positive employee and resident satisfaction surveys, a sharp decline in the number of regulatory issues (Figure 2), and gradual improvement in operational and financial performance (Figure 3). During a difficult time in the senior housing market Sunwest’s core assets performed on a par with or better than industry leaders (Figure 4).

Hamstreet & Associates’ third major task involved negotiation of agreements with secured lenders to provide breathing room for the reorganization. This undertaking was large on its face, involving more than 100 lenders (not including participants) and $1.5 billion of debt. Add in the lenders’ extreme hostility towards Sunwest and the national credit environment in 2008-2009, and the task may well have been impossible were it not for the intervention of the Securities and Exchange Commission. The SEC filed suit against Sunwest and its founders on March 2, 2009, leading—after a day in U.S. District Court and a week of follow-up negotiations—to an injunction that halted all foreclosures and other legal actions against the company.

The SEC suit also led to the creation of a federal equity receivership and appointment of a Receiver who worked alongside the CRO, handling areas such as claims administration and third-party litigation, and contributing jointly to development of the Receivership’s Distribution Plan.

Protected by the injunction, the CRO’s team continued debt negotiations on stronger footing, reaching an important agreement with GE, one of Sunwest’s two largest lenders, in the fall of 2009. At the same time, the CRO’s team disposed of Sunwest’s weaker assets and led the development of a restructuring plan that could win support from parties with extremely diverse interests. Working with investor representatives, the SEC, the Receiver, and special tax counsel, the CRO’s team created a plan to consolidate the core senior living affiliates into a unitary enterprise through the Receivership— restructuring the ownership and investment obligations as justified by the company’s rampant commingling of funds—then place the consolidated enterprise into chapter 11, restructure secured debt, and emerge as a healthy stand-alone senior living company. The plan also took investors’ tax needs into account.

From a situation that threatened to disrupt the lives of thousands of elderly residents and senior living employees, to return cents on the dollar to investors, Hamstreet & Associates engineered a truly dramatic and unexpected turnaround.

The CRO won support for the consolidated plan from GE and numerous investor groups during the summer of 2009. Other lenders began to support the process, too, as weaker assets were released from stay and stronger assets met adequate protection requirements. So successful did the eventual restructuring outcome appear, in fact, that the founder of Sunwest competitor Emeritus Senior Living and Columbia Pacific, Sunwest’s other major lender, approached the Blackstone Group seeking to form a joint venture to purchase the restructured enterprise. Most debt restructurings were consensual (99.2 percent), with a very small percentage accomplished through the Bankruptcy Code’s cram-down provisions (0.8 percent).

The offer from the Blackstone-Emeritus-Columbia Pacific joint venture came in September 2009 and sparked a new phase of the case. Through ensuing months, with the senior living operations running smoothly, the CRO’s team negotiated a tight purchase and sale agreement with Blackstone, obtained District Court approval of the Distribution Plan, consolidated Sunwest’s hundreds of affiliates into an existing chapter 11 proceeding, drafted the Plan of Reorganization and Disclosure Statement, and successfully completed restructuring negotiations to meet Blackstone’s challenging debt requirements. Blackstone won the stalking horse auction in May 2010, the Court approved the Plan of Reorganization in July 2010, and the CRO closed the $1.3 billion Blackstone transaction in August 2010.

From a situation in the fall of 2008 that threatened to disrupt the lives of thousands of elderly residents and senior living employees, to return cents on the dollar to investors, and to thrust responsibility for operating hundreds of senior living facilities onto lenders and/or state governments, Hamstreet & Associates engineered a truly dramatic and unexpected turnaround. Over the turnaround period, responsible cash management was restored, resident and employee satisfaction grew, operational and financial performance metrics improved, and hostile lenders came to trust the process. Tenant in common investors who might have received a few pennies on the dollar—like their counterparts in the collapse and bankruptcy of DBSI, another national seller of tenant in common investments—instead banked a 40 percent recovery on claims in December 2010, and expect another 20 to 25 cents on the dollar from future distributions.

The U. S. District Court publicly praised Hamstreet & Associates’ performance on two separate occasions, remarking via Court Order on “the high quality of the professional work and achievement” in the Sunwest Management case and stating: “The expected return in excess of 50 cents on MIMO claims is an outstanding result and is a credit to the ingenuity and dedication of many professionals and their firms. In particular, the Court recognizes that the CRO consistently provided the vision, judgment, leadership, and determination needed to maximize the value and return to claimants in this very complex and challenging case. . . . Hamstreet deserves recognition for the high quality and integrity of its work on behalf of investors and other claimants.” The Court also issued Hamstreet & Associates a certificate of appreciation.